Should I use my CPF for property purchase

Should I use my CPF for property purchase?

When purchasing a Residential Property in Singapore, the CPF board allows you to utilize funds in your ordinary account for your down payment and also the monthly installments. In Singapore, most home purchasers will choose to utilize as much CPF as they can, thinking that they cannot see, smell, and touch this money until they grow very old. However, things are not as simple as they seem; here are some points for you to consider.

1.Let your money work for you

One thing to note is that when you utilize CPF to pay for the house or monthly installments, you need to return all the CPF you have utilized, plus 2.5% per annum interest owed when you sell the property. On the other hand, if you had left this amount sitting in the CPF account, it would be earning you 2.5% interest per year. This is compounding interest, hence you will see the snowball effect after a period of time. What exactly does this translate to?

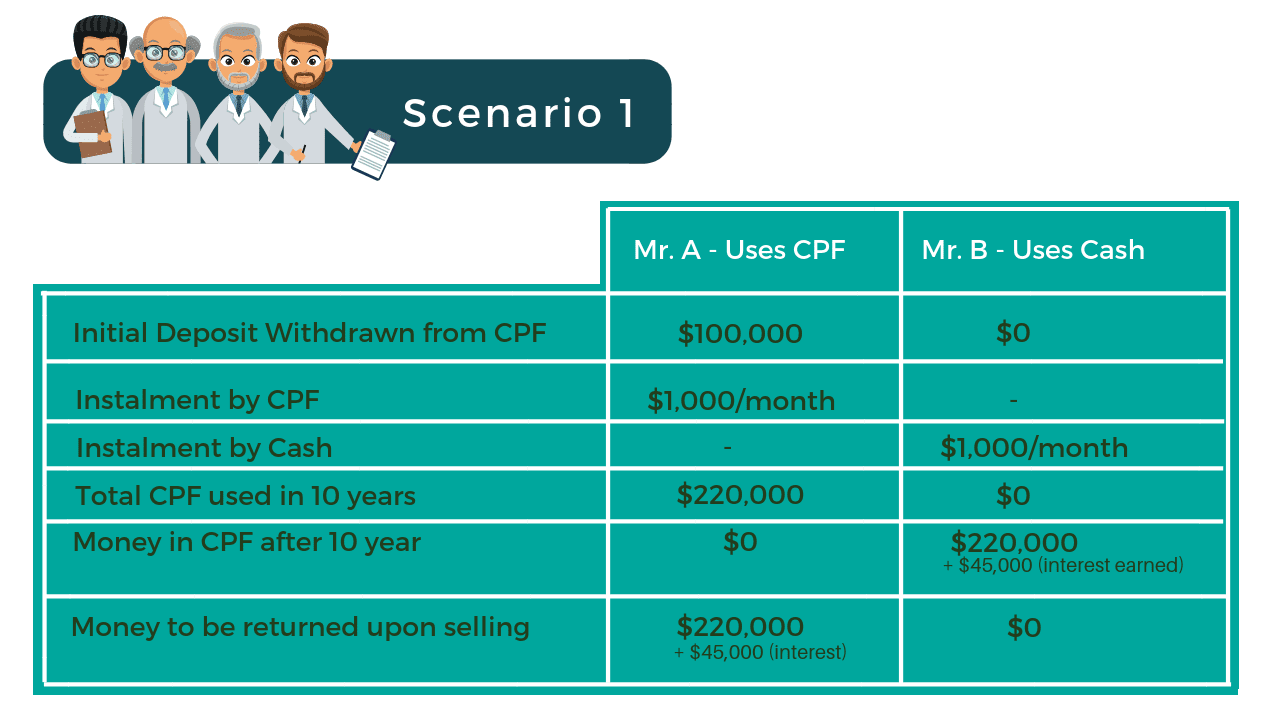

Let us take a look at the scenario below.

For simple illustration purposes, we will take a rounded figure of $100,000 CPF usage for the initial deposit for the property purchase and $1000 monthly CPF usage for loan repayment, over a period of 10 years.

In this example, Mr. A uses CPF to pay for both the deposit and monthly installments of the mortgage loan, whereas Mr. B uses cash for both. The total amount for monthly installments and deposits will be $220,000 after 10 years.

By then, when both property owners sell their house, Mr. B would have gained an additional $45,000 worth of interest in the CPF account, whereas Mr. A will need to return the $220,000 taken from CPF plus an additional $45,000 from the sales proceed.

The net result for Mr. B, who has not utilized CPF, will be that he gets $45,000 more cash from the sales proceeds, plus an additional $45,000 interest from the CPF funds. This makes him $90,000 richer in terms of cash flow.

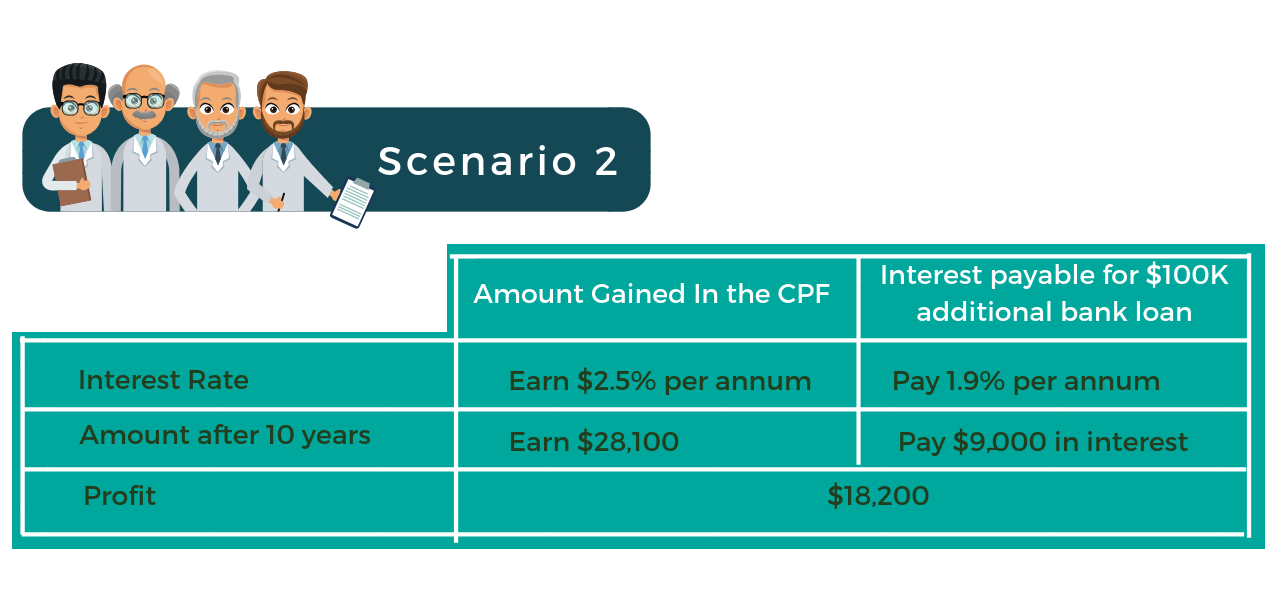

Scenario 2

Some home purchasers may wonder if they should use up all their OA savings or take up more bank loan. To illustrate this, we will use an example of taking up an additional $100,000 Bank loan and leaving this $100,000 inside of CPF.

If this $100,000 home loan is being charged at a rate of 1.9% per annum, the total interest payable after 10 years would be $9900, whereas a total of $28,100 worth of interest has been earned from the $100,000 inside of CPF.

So to borrow this additional amount of home loan and leave your CPF money inside CPF will net you $18,200 over 10 years. This strategy will make sense, assuming that the bank loan interest rates are lower than the interest rates that CPF is offering you.

Of course, in the event that Bank loan interest rate rises above the CPF rate, you can always utilize your CPF savings in addition to the accrued interest and pay down the loan.

2.Safety Net and Flexibility

The world we live in is every changing and always unpredictable. What happens if there is another financial market meltdown and you become unemployed? Imagine if you had left $100,000 inside your CPF; you can always use the amount plus the interest earned in order to pay you monthly instalments.

How many months’ installments can you pay with that buffer amount?

This will reduce the stress and financial strain in such hard times, enabling you to weather difficult times.

Another point to note is that you can choose to pay down with your CPF at any time when circumstances change (after the lock-in period, if there is one) so there is no need to hurry when you can simply let your money work for you.

Lastly, how much you utilise from CPF for your property will affect how much you can borrow in the event that you wish to do a cash out on your property. For example, when a person wishes to take an additional equity or term loan, the maximum amount will be affected by the CPF usage.

3.CPF for retirement

The interest rates that the CPF gives are relatively stable with no lock-in times or fees involved. Up to the first $20,000, CPF gives out an additional 1%, making it 3.5%. This is considered quite a good rate in Singapore, given that there are no other criteria and at such low risk. The original purpose of the CPF account is to help one grow their retirement fund in a disciplined manner. We often neglect planning for the future while we work hard and spend on our current lifestyle.

Conclusion

To sum up, in most cases it will be wiser to leave the CPF in its account for the 3 reasons above. However, in the scenario where you need the cash flow and would like to utilize the CPF for the monthly installments, there is nothing wrong with that either. Likewise, if you are a savvy investor and would prefer to use your cash on other investments that can earn a better rate than the CPF, it will be great to do so too.

For more personalized info, feel free to speak to one of our expert home loan experts by contacting us at (+65) 6631 8980 (main line).

{kind=link}